The recent Five Presidents' Report set out a number of steps to further strengthen the EU's Economic and Monetary Union (EMU). One of the key deliverables under the first stage of the Completion of the EMU is to move towards a European.....

Deposit Insurance Scheme (EDIS) as a further step to a fully-fledged Banking Union. EDIS would mark an important step towards reinforcing financial stability by further weakening the link between banks and their national sovereigns and by delivering even greater trust in the safety of retail bank deposits, regardless of a bank's location in the Union.

The Commission's legislative proposal on 24 November 2015 introducing EDIS will strengthen the protection of bank depositors across the Banking Union. EDIS would develop over time and in three stages: first a re-insurance stage, then a co-insurance stage and, finally, a full European system of deposit guarantees, which is envisaged for 2024. The Commission's proposal is accompanied by a Communication which sets out other concrete measures to further reduce remaining financial stability risks in the Banking Union.

2. How does EDIS fit within the Banking Union?

In 2012, the European Council agreed on a roadmap for completing EMU based on deeper integration and mutual support. Completing the Banking Union is an indispensable step to a full and deep EMU. The first pillar of the Banking Union[1] consists of a common framework for supervision of banks to be implemented by the Single Supervisory Mechanism (SSM); the second pillar consists of a common framework for bank resolution to be implemented by the Single Resolution Mechanism (SRM). Those two pillars have been put in place. The third pillar, a deposit insurance scheme, is still needed and needs to be put forward now. In contrast to the situation in 2012, the European banking sector is on a much more solid footing, following the introduction of more stringent capital and liquidity rules and centralised supervision and resolution.

3. Why do we need EDIS now?

EU legislation already ensures that all deposits up to €100 000 are protected, through their national deposit guarantee scheme (DGS), in case of a bank failure. However, national DGS can be vulnerable to large local shocks. EDIS provides a stronger and more uniform degree of insurance cover for all retail depositors in the Banking Union, ensuring that the level of depositor confidence in a bank would not depend on the bank's location.

Any divergences, perceived or real, between national DGS can contribute to market fragmentation by affecting the ability and willingness of banks to expand their cross-border operations. EDIS would ensure a level playing field for banks across the Banking Union by reducing the vulnerability of national DGS to large local shocks, weakening the link between banks and their national sovereigns, and boosting depositor confidence overall.

In the Banking Union, EDIS would increase the resilience of the banking sector against future crises and contribute to financial stability. Ultimately, greater confidence in bank deposits would enable greater lending to the economy, meaning more growth and jobs for Europe.

4. What is the European Commission doing to reduce banking risks?

The Commission's proposal for EDIS seeks to deepen EMU and to weaken the link between banks and their national sovereigns by means of risk-sharing among all the Member States in the Banking Union. However, this risk-sharing must be accompanied by risk-reducing measures that are also designed to break the bank-sovereign link. Therefore, the proposal is accompanied by a Communication, which sets out other measures to further reduce risks and ensure a level playing field in the financial system.

- The Commission's first priority will be to ensure full transposition by Member States of existing legislation in this field, such as the 2014 Directives on Bank Recovery and Resolution (BRRD) and on Deposit Guarantee Schemes. Infringement proceedings against the relevant Member States are ongoing.

- Second, the Single Supervisory Mechanism must be able to operate as effectively as possible by reducing and aligning national options and discretions for banking prudential rules. We are working with the SSM to take steps to eliminate the remaining national options and discretions in EU banking legislation and to reinforce the single rulebook. This means that the same rules and supervision will apply to all banks.

- Third, we will further reduce the possibility of resorting to taxpayers for failing banks. We will bring forward legislation for adequate loss-absorbing capacity resources for banks and will implement the recently agreed international standards by the Financial Stability Board by 2019.

- Fourth, we will vigorously enforce EU state aid rules to minimise the use of public funding to maintain a solvent and resilient banking sector.

- Fifth, we will work to increase clarity and predictability by converging insolvency law as set out in the Capital Markets Union Action Plan.

- Finally, a number of further targeted prudential measures to address weaknesses will be dealt with by implementing the remaining elements of the regulatory framework agreed at international level, in the Basel Committee on Banking Supervision (for example: measures to limit bank leverage, to assure stable bank funding, and to improve the comparability of risk-weighted assets.)

The Commission will ensure that good progress is made on further measures to reduce risk, in parallel with the establishment of EDIS by 2024.

5. What does EDIS entail?

EDIS would be administered by a Single Resolution and Deposit Insurance Board ("the Board" [see question 17],) part of the Single Resolution Board, as the body entrusted with decision-making, monitoring and enforcement powers relating to the EDIS framework. A European Deposit Insurance Fund would be established to insure national deposit guarantee schemes (DGS). National DGS would remain in place and would be part of EDIS. They would retain an important role in particular in the initial stages (re-insurance and co-insurance - see question 8). They would be first in line to cover pay-outs in the re-insurance period. In the co-insurance period, coverage of deposits would be shared between the Deposit Insurance Fund and the national DGS.

6. Which deposits would be protected by EDIS and in which scenarios?

Together with the national deposit guarantee schemes (DGS), EDIS would cover deposits below €100 000 of all credit institutions which are affiliated to any of the current national DGS in the Banking Union. In the first stages of EDIS (re-insurance and co-insurance - see question 8), funding would be shared between the Deposit Insurance Fund and the national participating DGS. The share of funding provided by EDIS in case of a pay-out would progressively increase. In the final stage (full EDIS [see question 8]), EDIS would fully fund pay-outs in the event of bank failures.

EDIS would intervene in two scenarios (along with the national DGS in the first two stages of EDIS):

- A) when a failing bank is liquidated and deposits need to be paid out, and

- B) when a failing bank is resolved and the transfer of the deposits to another institution needs to be financed so that deposit access is not disrupted.

7. What is the scope of EDIS?

Every deposit-taking bank established in the Banking Union would be covered by EDIS. The scope of EDIS corresponds to that of the Deposit Guarantee Schemes Directive[2]. The proposal does not exclude any group of deposit-taking banks, irrespective of the type of Deposit Guarantee Scheme (DGS) to which they belong. This means that statutory DGS, but also institutional protection schemes and contractual schemes, are covered if these are recognised as a DGS. Nevertheless, contributions by banks to EDIS would be risk-based and would take into account both the relative probability that they would require the activation of deposit insurance and the amount of deposits that would need to be covered. This risk profile would become more significant when this calculation switches to a European basis at the start of the co-insurance phase.

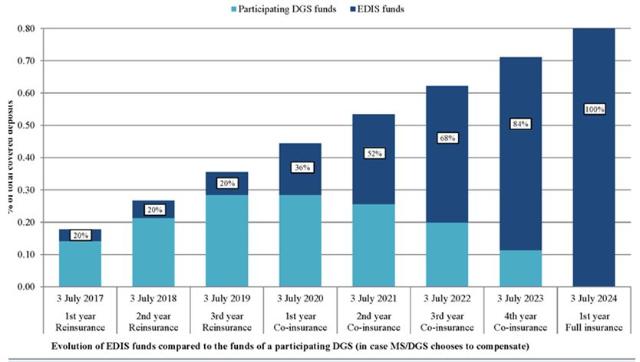

8. What are the different stages of EDIS and how does EDIS sit alongside national DGS in those stages?

Currently, all Member States have deposit guarantee schemes as the Deposit Gurantee Scheme Directive requires all deposit-taking banks in the EU to be a member of a national DGS. National schemes would continue to co-exist alongside EDIS. EDIS would be established in three sequential stages:

- The first stage would be a re-insurance scheme and would apply for 3 years until 2020. In this stage, EDIS would provide a specified amount of liquidity assistance and absorb a specified amount of the final loss of the national scheme in the event of a pay-out or resolution procedure. In order to limit moral hazard and avoid “first-mover advantages”, a DGS can only benefit from EDIS in this stage if it has met its requirements and filled its national fund to the required level, and only if those funds have been fully depleted. There are also robust safeguards to avoid any possible abuse of the system [see question 11].

- The second stage would be a co-insurance scheme and would apply for 4 years until 2024. For this phase, a national scheme would not have to be exhausted before accessing EDIS. EDIS would absorb a progressively larger share of any losses over the 4-year period in the event of a pay-out or resolution procedure. Access to EDIS would continue to be dependent on compliance by national DGS with the required funding levels.

- In the final stage, EDIS would fully insure deposits and would cover all liquidity needs and losses in the event of a pay-out or resolution procedure.

While the re-insurance and co-insurance stages would share many common features, ensuring a smooth gradual evolution, the costs for covering deposits would be increasingly shared among the national DGS and EDIS under the co-insurance stage. The full insurance of depositors in the Banking Union would fall under EDIS from 2024 onwards.

9. How can 're-insurance' break the bank/sovereign loop and restore financial stability?

In the re-insurance stage, EDIS would only provide an additional source of funding to that of the national DGS, thereby only weakening the link between banks and their national sovereign to a limited extent. That is why the re-insurance stage is only a first step and would be followed by progressive mutualisation of deposit insurance cover during the co-insurance stage, leading to full insurance in the final stage.

10. How would EDIS transition from re-insurance through co-insurance to full insurance?

The transition between the three stages of EDIS would take place automatically. After an initial period of 3 years, the re-insurance stage would convert to a co-insurance stage and ultimately into a full insurance of national deposit guarantee schemes.

11. How would EDIS be triggered?

There are three steps:

1st step (Alert)

A DGS alerts the Board about circumstances that are likely to lead to a bank failure. The Board can prepare itself so that it can quickly provide any necessary funding to the DGS if the bank fails and the DGS has to pay out to depositors or contribute to a resolution procedure.

2nd step (Notification and trigger)

If a DGS is required to compensate depositors or contribute to a resolution procedure, the Board would decide within 24 hours whether the conditions for EDIS support are met and about the amount of funding that would be provided. The Board would provide EDIS funds immediately after taking such a decision.

If several bank failures occur simultaneously and the European Deposit Insurance Fund is insufficient, the Board could also decide to provide funding on a pro-rata basis.

3rd step (Monitoring, repayment and loss cover)

After the Board has provided EDIS funding to a national DGS, it would closely monitor the use of the funds and ensure that the DGS repays EDIS on a pro-rata basis from any proceeds it receives from the insolvency estate of the failed bank.

12. What are the safeguards for accessing EDIS?

Various safeguards are built into the system to ensure that the right incentives are in place for national DGS to reduce costs and risks.

In particular, there are three conditions that must be met in order to access EDIS funding:

- The yearly target levels that a national DGS must reach in order to claim EDIS funding. In other words, a DGS cannot claim funding from EDIS unless it has fully raised what it should have raised each year by complying with the obligations in the DGS Directive, and complies with other key provisions of the DGS Directive.

- During the first two phases, the DGS must always bear a part of the burden itself: during the re-insurance stage, the DGS must first exhaust its own funds before seeking EDIS funding; during the co-insurance stage, a DGS would bear part of any losses from a pay-out or contribution to resolution itself.

3. Following a pay-out event, a national DGS must ensure that it maximises the proceeds from the insolvency estate of a failed bank and repay the Board accordingly. The Board has sufficient powers to enforce these rights. If a DGS has not complied with its obligations, all or part of the EDIS funds received would have to be repaid.

13. Will EDIS penalise those national DGS which have already significant resources?

No. First, only a deposit guarantee scheme (DGS) which has raised what it should have raised each year by complying with its obligations under the DGS Directive can access EDIS. The Regulation sets annual targets with which the DGS must comply.

Second, the national DGS will not receive less funding because they exceed the funding levels required under the Directive. In the re-insurance phase, national DGS will only need to exhaust the amount of funds which they should have collected under the Directive before accessing EDIS, but not those funds which they have collected in excess. In the co-insurance phase, access to EDIS will not depend on the exhaustion of available national funds.

14. How big would the Deposit Insurance Fund be and how much would banks contribute to it?

The Deposit Insurance Fund would be equivalent to 0.8% of the covered deposits of all banks in the Banking Union by 2024. In absolute terms and based on data from 2011 on banks’ balance sheets, the fund would reach around €43 billion. The target size of the fund would be dynamic and increase automatically if the banking sector grows. The Fund would be gradually built-up over a period of 8 years.

The banking sector would contribute annually a total of around 12.5% of the target amount to the respective DGS and EDIS, or about €6.8 billion in absolute terms, until the Fund is filled.

The precise amount that an individual bank would need to contribute would be determined by a delegated act and take into account the risk profile of a given bank.

DG FISMA, 2015

15. How would EDIS be funded?

Banks would finance EDIS via ex-ante contributions. The ex-ante contributions to EDIS are separate from banks' obligation to pay ex-ante contributions to their DGS under the DGS Directive. In order to achieve cost-neutrality for the banking sector, the ex-ante contributions paid to EDIS will count towards the national target level set by the DGS Directive.

16. Would EDIS increase the costs of banks?

There would be no extra cost to the banking sector by switching to EDIS. The target level of 0.8% of covered deposits set by the Deposit Guarantee Scheme (DGS) Directive remains, but contributions to EDIS would count towards the target level of national DGS.

Regarding the individual contributions of banks, these would vary depending on their risk profile. The risk profile would continue to be set at national level compared to all banks in a Member State and should stay stable during the re-insurance phase, and would be set at European level compared to other banks in all participating Member States as of the co-insurance phase. Overall, EDIS would not impose an additional cost for the banking sector in any of the phases.

17. What about the transitional phase where national deposit guarantee schemes are not fully funded?

EDIS would be built up over a period of 8 years. Nevertheless, EDIS would provide assistance from the start in the form of re-insurance. EDIS interventions would be limited to 20% of its initial target level or 10 times the target level of the national DGS (whichever is lower) in order to protect its limited funds in the beginning. Loss participation of EDIS would increase over time as funds are built up.

18. How would contributions to the European Deposit Insurance Fund be calculated?

Contributions would be based on covered deposits and a bank's own degree of risk. The calculation would be made so as to ensure that the contributions of all of the banks amount to EDIS's annual target level. The criteria for the calculation would be specified in secondary legislation, which would be adopted by the Commission in a delegated act.

19. Who would manage EDIS?

A strong and independent authority at Banking Union level is needed to administer EDIS, decide on the risk-adjusted contributions from the banks, monitor contribution inflows and manage pay-out cases.

In the Commission's proposal, this role would be played by the existing Single Resolution Board(SRB), with an appropriately modified governance structure for its new DGS tasks. The Board would administer the Single Resolution Fund (SRF) and the European Deposit Insurance Fund together, thereby creating synergies when combining responsibilities for resolution and deposit insurance. This arrangement would establish the Board as the key first point of contact in a crisis, facilitating swift and decisive crisis management.

Triggering EDIS is subject to clear conditions and leaves only marginal discretion to the Board. In addition, appropriate measures will be put in place to manage any potential conflict of interest, in particular by segregating the Deposit Insurance Fund from the Single Resolution Fund. However, it may be necessary to address potential conflicts of interest by ensuring that the Deposit Insurance Fund would be appropriately segregated from the SRF.

20. What Happens To National DGS In 2024?

In 2024, in the full insurance stage, the national DGS would continue to stay in place in order to administer any pay-out events and to act as a contact point for depositors and banks. National DGS might also still collect funds in excess of the 0.8% of covered deposits, which would remain in the national scheme.

21. Why is an Intergovernmental Agreement (IGA) not necessary for EDIS?

For the Single Resolution Mechanism, at the request of the Council, certain elements related to the functioning of the Single Resolution Fund, namely the transfer of the contributions collected by the national resolution authorities to the Fund and the mutualisation of the financial resources available in the national compartments, are regulated in an Intergovernmental Agreement (IGA) between the participating Member States.

The proposed EDIS has a very different set up than the SRM. It consists of a system of insurance starting with a re-insurance of national DGS, financed by direct contributions from banks to the European Deposit Insurance Fund.

The EU Treaty provides a sufficient legal basis for this proposal. When setting up a Single Resolution Fund (SRF) for the Banking Union, there was a need to provide for a transfer of funds from national resolution funds to the SRF from the very beginning. However, in the case of EDIS, banks contribute directly to the European Deposit Insurance Fund. Therefore, an IGA is not necessary as there is no transfer of funds already collected by a national DGS to the European level.

22. Risk Reduction

A. The Commission will work to ensure that further measure to reduce risk are taken in parallel with ongoing work to establish EDIS, including any necessary regulatory changes. Why is it necessary to further reduce national options and discretions in the application of prudential rules?

During the first year of the SSM, substantial progress has already been made in eliminating options and discretions in prudential rules that apply to banks in the Banking Union. Nevertheless, the ECB has recently identified over 150 options and discretions and launched a public consultation on harmonising the exercising of supervisory options and discretions within the Banking Union. The inconsistent exercise of options and discretions can contribute to fragmentation and risk in the banking sector. This can lead to legal uncertainty and makes it more costly for banks to operate within the Banking Union. Institutions may even exploit regulatory differences and thereby distort competition. Furthermore, in the Banking Union the impact of risks generated under certain nationally implemented rules will likely not be contained to that country, but have effects across the Banking Union.

B. Are changes necessary to the framework for resolving failing banks?

The Single Resolution Board has been working since March 2015 and will be fully operational as of January 2016. It is essential that the Board has all means at hand which are necessary to respond in a timely and effective manner if a bank is failing or likely to fail. To avoid costs to the taxpayer, it is key that enough “bail-inable” liabilities are available. Hence, implementation of the “minimum requirement for own funds and eligible liabilities” (MREL) will be crucial. In addition, the Financial Stability Board (FSB) has developed a requirement for a Total Loss Absorbing Capacity (TLAC) at global level to ensure globally systemic important banks have sufficient capacity to absorb losses. The Commission will bring forward a legislative proposal in 2016 so that TLAC can be implemented by the agreed deadline of 2019. This will be another step towards harmonising minimum requirements.

C. How do you ensure that the taxpayer will be better shielded from crisis costs in the financial sector?

As part of the SRM, a Single Resolution Fund (SRF) has been established which pools significant resources from bank contributions and therefore protects taxpayers more effectively from the cost of crisis in the financial sector. During 2015, banks have been contributing to national resolution funds. In 2016, banks in the Banking Union will start to contribute to the SRF.

Equally important, there must be a consistent application of the bail-in rules under the BRRD to ensure that the costs of resolving banks are primarily borne by their shareholders and creditors. This is a pre-requisite to the use of the SRF or public funds. Decisions to use funding from these sources are subject to EU State Aid and Fund Aid rules. These will continue to be enforced to ensure that the use of public money is minimised and aided banks are viable.

D. Is there a need for more harmonisation in insolvency law and restructuring proceedings?

Yes, the Commission believes there is a need for greater convergence in insolvency law and restructuring proceedings across Member States. This has been identified in the Commission’s Action Plan on Building a Capital Markets Union of 30 September 2015. The divergence in insolvency laws impede the management of credit risk and may impede resolution action. The Commission will consider bringing forward proposals for enhancing legal certainty and encourage the timely restructuring of borrowers in case of financial distress. These measures should be particularly suitable to enhance the prospect for success of strategies to manage non-performing loans (NPLs). The issue of NPLs will also be brought up in the context of the European semester, where the Commission will call for measures by Member States to settle NPLs, including the upgrading of insolvency regimes towards best practices.

E. Are new prudential measures needed?

As a response to the financial crisis, the EU has put in place a comprehensive framework of rules on capital requirements and risk management for financial institutions. At the global level, this is commonly referred to as ‘Basel III’, as agreed by the Basel Committee. Nevertheless, a few further targeted prudential measures still need to be put in place. These measures include the limitation of bank leverage, assuring that banks have stable funding sources and to improve the comparability of risk-weighted assets. Work in these areas is currently ongoing within the Basel Committee and the Commission intends to make proposals for amendments to the CRDIV/CRR.

Finally, the adequacy of the prudential treatment of banks’ exposures to sovereign risk should be re-considered. Work on these matters is currently underway at the international level. In this context, the Five Presidents’ Report refers to the possibility of the introduction of limits on banks’ exposures to individual sovereigns, as a means to ensure that their overall sovereign risk is sufficiently diversified. The Commission will come forward with the necessary proposals on the prudential treatment of sovereigns, drawing on quantitative analysis under preparation in the Economic and Financial Committee and the Basel Committee and paying particular attention to financial stability aspects

6 commenti:

Paolo...e' impossibile...perfino in Grecia hanno salvaguardato u conti correnti...ripeto..se non fosse garantito uno e uno solo dei conti correnti ci sarebbero le file agli sportelli...

Questa roba è una follia

...e nel frattempo la Merkel ha dichiarato, pochi giorni or sono, che la Germania non vuole partecipare alla garanzia europea sui depositi inferiori a 100.000 euro; quindi, quando falliranno le prossime banche italiane, non solo verranno depredati gli azionisti, gli obbligazionisti subordinati e senior ed i correntisti sopra i 100.000 euro, ma se il fondo di tutela dei depositi non è sufficiente e non viene implementato EDIS, anche i conti correnti sotto i 100.000 sono a rischio ...

in proposito segnalo un interessante e controverso articolo di Luca

Davi sul sole 24ore del 13 dicembre dove l'autore asserisce, con argomentazioni logiche e tecniche, che le prime 10 banche italiane non attiveranno mai il bail in poiché non ne ricorreranno mai i presupposti, vale a dire non preoccupatevi, i vostri conto correnti anche sopra i 100.000 euro, in queste 10 banche, non saranno mai intaccati, anche in caso di bail in.....

per correttezza va detto che la legge BAIL IN esiste anche in svizzera, dove i correntisti sono tutelati sino a 100.000 chf anche se vi sono banche cantonali che, almeno per ora, tutelano con garanzia dello stato l'intero ammontare dei depositi.....

in ultimo, presumo che il povero Lopresto avrà di sicuro ricevuto anche una visita del nucleo valutario della guardia di finanza per spiegare che fine ha fatto quel 1.500.000 di euro....

caro anonimo delle 19.14 sei un.... leggero!!!! non so se avete notato: cipro, grecia, ora da noi Banca Etruria.... cosa hanno in comune? ve lo dico, SONO TUTTI BAIL IN DIFFERENTI, perchè le decisioni vengono tarate su dove sono i soldi. Per l'Italia, paese populista per eccellenza, vedo, nel caso di un grande gruppo che rischia un bail in totale, un bell'aggio stile patrimoniale su TUTTI ( e magari salvano le subordinate che la gente sta vendendo a piene mani ) 10-15 per cento, cosi fanno pagare anche chi ha soldi in posti meno pericolosi, che, quando si tratta di sistema italia, è tutto relativo. e come diranno loro, "abbiamo messo il sistema bancario in sicurezza"

Anche i greci dicevano 3 anni fa: non succederà nulla ...state e stiamo tranquilli.....col bancomat abbiamo sempre i soldi a disposizione ...ed in banca ci conoscono........Poi si è visto! (Un saluto al Sig.Barrai)

Tutta colpa di chi vuole tornare alla lira.

L'euro è di per sé una garanzia.

Io da quando c'è l'euro, posso spostare i miei risparmi dove voglio, pagando ovviamente tutte le tasse dovute in Italia attraverso regolare modello unico, con l'ausilio del commercialista.

Peggio per i c....oni che piazzano i loro averi nella prima banca che gli capita e agli avidi che portano i loro soldi all'estero in nero pur di pagare qualche tassa in meno.

Bail in e fine del segreto bancario la prospettiva per un radioso futuro.

Posta un commento