NOI DI MERCATO LIBERO NE PARLIAMO DA ANNI. QUESTO BREVE ARTICOLO SPIEGA IN DETTAGLIO COME UNA QUALSIASI MINI ATTIVITA' POSSA FINANZIARSI GRAZIE ALLE CRIPTOVALUTE!

E POI DICONO CHE E' UNA BOLLA??? LA BOLLA E' QUELLA DELLE BANCHE CENTRALI. QUA SI STA CREANDO RICCHEZZA VERA E FATTA PER RIMANERE

Laundry Tokens

Imagine

we are industry experts in providing laundry services, and we publicly

announce a plan to open a new chain of laundry shops, where the

development will be funded through an ICO process. The tokens would be

issued at a price of 1 Laundry Token (LTX) for $1 and will enable

holders to gain access to laundry services in all laundry shops that are

a part of the new chain. However, we will only ever issue 1 million

LTX, thereby creating artificial scarcity.

In addition, this will be done through an independent third party to

ensure we are unable to defraud the system i.e. the independent third

party will ensure that we cannot issue more LTX and or recall LTX

already issued to people, and ensure the LTX already issued will be

honored for their intended purpose. Furthermore, imagine that the LTX

price can go up and down based on supply and demand, and that they are

easily transferable between users at the fair market rate. Under the

efficient market hypothesis, the value at which the tokens are exchanged

in a sufficiently liquid market will capture all the market information

relating to the underlying project. The theory is that as we issue the

LTX token and use the funds to build the laundry business, the value of

the LTX will go up (on anticipation of a successful launch) and so LTX

holders will enjoy the benefits of capital gains. On the other hand if

the project begins to struggle and bad news enters the media, the value

of the LTX will begin to decrease and LTX holders will suffer capital

loss.

In

order to ensure that the economics of the LTX works as an appcoin the

issued tokens need to be convertible for their intended purpose of

receiving laundry services i.e. holders should be able to take their LTX

to any of the shops in the laundry chain and pay for required services.

LTX can be divisible into subunits, but for simplicity in this example

when a single LTX token is redeemed in a shop it is converted to laundry

credits equivalent to the market rate in USD. Therefore, if 1LTX is now

being traded for $50, then on redemption at the shop the holders can

gain access to $50 of cleaning credits e.g. they can clean five jackets

where the cost of cleaning is $10 per jacket. As the value of the tokens

goes up, on the open market, holders can gain more laundry credits “for

free” on redemption i.e. more jackets cleaned for the same units of

tokens.

A token’s Monetary Policy means the model for supply release and the cap

on total supply i.e. how many tokens are issued and how often, and what

the total number of issued tokens will be. A capped and well-controlled

supply release increases the chances of a small increase in demand

driving token prices higher. Normally the monetary policy would be

pre-defined as part of the issuance strategy, where a fixed number of

tokens are created and issued. However, even though there is a total

supply cap the issuer would only distribute a certain fraction of the

available tokens to raise a fixed amount of capital for executing the

business plan. The remaining tokens are then held in an “escrow” type

service to finance operational costs or future connected projects. For

example, in the previous case of the laundry LTX ICO the supply was

capped at 1 million tokens, and then we may only distribute 500k LTX

tokens and keep the remaining in an escrow account, which we can use to

cover costs of running the business and or expanding laundry shops in

the future. The escrow account would likely have some form of

access/usage controls to provide comfort to investors that the tokens

held will not be dumped (sold in one go), in turn causing a price crash;

or they may be locked for a fixed period to allow sale in a controlled

manner over a “sufficiently long” period of time. All of these aspects

fall under the monetary policy of a token as they are related to

directly managing the supply of tokens in circulation, and is a

relatively well-understood concept in cryptocurrency.

Fiscal Policy

It

is also important to understand and define the commercial benefits the

ICO participants gain from holding tokens, beyond just the capital gains

related to scarcity. This point is a key one, and one that is least

talked about and or understood, but is just as important as a token’s

monetary policy. In the case of the laundry ICO earlier, as we are

ultimately developing a business we want to maximize the value being

created so we will potentially offer laundry services in the issued LTX

but also in USD fiat currency (and even in other cryptocurrencies BTC,

ETH and ETC). Linking a commercial benefit (e.g. discounts) with token

usage means customers would be more likely to access our services

through LTX rather than any other form of payment, this is especially

true if there is a large supply of tokens in circulation (resulting in

less scarcity).

To

drive continued customer interest in buying LTX, as issuers we can

ensure that LTX holders always gain some benefits/discounts on the

services offered e.g. rather than cleaning costs for a jacket being $10

the LTX holders may only pay $8. This discount may be adjustable so we

can manage commercial benefits based on levels of external competition,

changes in operational costs and other unknown factors. This becomes a

way of managing the flow of the issued token without taking drastic

actions related to monetary policy e.g. increasing/decreasing supply

from circulation or even hoarding/dumping tokens. This control of flow

of tokens and impacts on aggregate supply and demand is a form of

“Fiscal Policy”. The fiscal policy actions highlighted in this paragraph

are not directly connected to managing the supply of tokens in

circulation but rather connected to managing the flow of tokens through

indirect economic incentives.

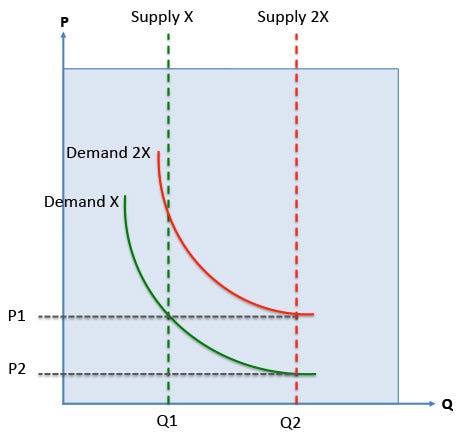

One

example of a potential use for such a fiscal policy mechanism is that

an issuer can propose to increase the commercial benefit (e.g. cleaning

discount in LTX), which will increase aggregate demand of the tokens

(from D1 to D2 in diagram below). Such an action can then be combined

with monetary policy decisions, for example as the aggregate demand of

the tokens increases through the fiscal policy decisions, the issuing

company could then also release further tokens, that may be held in

escrow, increasing the total supply in circulation (from S1 to S2 in

diagram below). This combined increase of supply in circulation and the

demand due to increased commercial benefits may have a minimal impact on

the current market price. This simple thought experiment can be

visualized as in the following diagram:

This

model, taking into account monetary and fiscal policies (which are

fundamental in macroeconomics), and applying a framework, which allows

them to interact, and effect aggregate supply and demand, shows how

critical these policies are to understanding ICO structure, appcoins,

and their impact on future issuing projects/companies and the capability

for value creation and risk causation for token holders

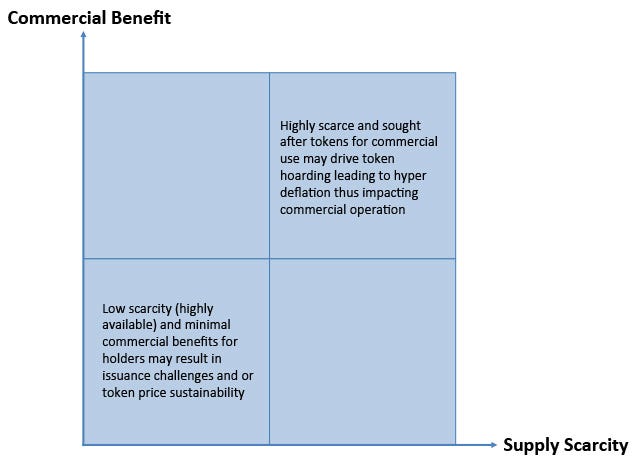

Supply and Demand

As

seen above, from a monetary policy and fiscal policy perspective, the

balance of Commercial Benefit and Supply Scarcity factors is critical in

planning the issuance of a sustainable appcoin and the impacts on a

business (see the diagram below). The economic analysis for such a

balance can be modeled through assessing the supply and demand surfaces

based on these explanatory factors. As a thought experiment it is viable

to assume that highly scarce tokens with very high commercial benefit

(e.g. offering steep product discounts) may result in hyper deflation of

their value, leading to a hoarding mentality, as there will be a view

of “falling prices” or being able to purchase more with the same tokens

if they delay redeeming. While this may seem like a positive effect, as a

higher purchasing capability of a token implies higher returns for a

company when they sell a redeemed token back into the market, such a

scenario also has the potential to detrimentally impact a business and

its cashflow. One of the most obvious impacts is that whilst a hoarding

mentality will result in people delaying the use of their tokens,

accordingly customer perceptions of using fiat currency to pay for

services could cause them to feel like they are getting a worse deal

compared to buying with a token, hence driving them to also delay their

purchase, or using substitutes and or competitive products/services.

This business slow-down will, in turn (assuming an efficient market),

lower the value of the token until an equilibrium point is reached.

However, the equilibrium point may not be what makes this a highly

profitable business. On the other hand, tokens with low scarcity and

minimal commercial benefit may be of little interest to users either as

“investments” or for access to services. Evidently there is a level of

complexity here that is very challenging to assess without some historic

and forecast sales revenue/cost data related to a company’s core

product or service and its customer profiles.

The Optimal Model

From

an issuer perspective, as the tokens are redeemed by holders for their

relevant commercial purposes, for which they may receive company credit

(e.g. coat cleaning in the laundry example) the company can resell the

token in the market at the current market rate. Using this approach the

company can recover operational costs and generate profits. This cycle

of token purchase and redemption by customer and resale into the market

by issuer can continue, meaning the appcoin tokens would become a form

of money that is only locally accepted by the issuing company. From this

context it becomes apparent why the above framework considering

monetary and fiscal policies and their interactions makes sense, as “a

long line of research emphasizes that separating monetary and fiscal

policies overlooks policy interactions that are important for

determining equilibrium” [15].

As

an appcoin model, the above may be the most viable basic structure

making business and economic sense. Conversely, an example of a

nonsensical token structure would be a 1-to-1-access model wherein the

issued tokens are just for single-use only, then their market value

would intrinsically be capped at the value of substitute offerings. For

example, if 1 token represents 1 unit of service, and competitors charge

$10 for the same service (all other things being equal), then it is

irrational for token purchasers to pay more than $10 for one token on

the open market (assuming no commercial discount for token holders).

In

addition, issuers must account for the time it takes to sell the token

in the open market after being redeemed by a holder for its intended

commercial purpose. In a sufficiently liquid market this may be

“instantaneous”, thereby minimizing the risks associated with price

volatility. From a commercial perspective these risks could be severe

because hoarding tokens to control market supply may backfire if token

value falls. In this scenario the issuing business may not be able to

sell the tokens it holds to recover costs incurred delivering the

services in return for redeemed tokens. While risks can be hedged if

appropriate instruments/services are available, the optimal model would

see smaller companies refrain from hoarding, instead preferring to sell

in sufficient quantities to at least recoup costs. This is also the

model used by blockchain miners.

Leading

on from this is the challenge of “retiring” tokens, for example if an

issuing organization at some point in the future decides to discontinue a

particular product/service, or move away from a token model. In this

scenario the token holders can effectively be seen to have some form of

right or vote on the future of the product or service offered by the

company! This challenge becomes greater than just a simple vote because

as the value and or usage of these tokens increases, the holders will be

seen to have more influence over company decisions. The optimal and

simplest approach would be for the issuing company to buyback the tokens

from holders at the market rate; a process which must be managed

appropriately so that any announcements and buyback processes will not

result in liabilities for the company. In this context, it must be noted

that retiring any form of “money or security” from circulation (if

these appcoin tokens are thought of as such) is a huge challenge. On a

much larger scale this is evident in the issues that occurred in India

with the heavy-handed banknote demonetization strategy in 2016 [14].

In the case of an appcoin the scale would be much smaller, but as a

company grows and token values and or usage increases the challenges

could be similar, especially when the tokens represent some form of

access to a product or service that people have become attached to, or

is critical to operations for which they still require some form of

support from the issuing company (think Windows XP). A prudent way to

manage this would be to have a buyback/demonetization strategy as part

of an appcoin ICO, and even some functionality to manage this

autonomously in a controlled manner.

Viable and non-Viable ICOs

Executing

an ICO, issuing appcoins and managing the micro/macro-economic impacts

on the business, key stakeholders and the market will mean companies in

the future may not only need a CFO but likely also a Chief Economist, as

running such a firm will be akin to running a small country! This will

be more of a problem for a startup or a fledgling company, but maybe not

so for an ICO executed by a larger firm with a more established product

or service.

If

a large, established company e.g. Spotify, Netflix, and even PornHub

(which is probably the most likely considering the history of

pornography and its influence in driving the uptake of new innovative

business models [15]),

executed an ICO and issued an appcoin, for managing operating costs or

expansion of services, it may make commercial and economic sense to do

so. In this scenario the economics can likely be modeled with an

acceptable level of confidence due to good availability of sufficient

historic and forecast operational and financial data. Therefore, an

appropriate token structure can be setup and deployed for the ongoing

benefits of participants and sustainability/growth of issuer’s business

model.

In

a startup context an appcoin ICO would likely only make sense

commercially/economically for a series A (or greater round) when a

decent product-market fit has been defined and scale up capital is

required. From this context it can be seen how an appcoin ICO model may

even be hugely disruptive for later stage venture capital firms,

contrary to their current views [16]!

In

either of these cases, for established companies and or scale-up firms,

the key question then is why use an ICO on a public blockchain if the

appcoin tokens are not securities? If appcoins are not securities and

they can be easily and widely marketed to retail investors, and the

token life cycle can be managed without the challenges of complex client

money and asset rules, why use a smart contract blockchain to execute

an ICO? Why not just use cryptocurrency payments (or any form of

payments) with the appcoin mechanism managed through a centralized

system?

Some Legal Aspects

No

discussion on ICOs would be complete without providing some legal

points of views. We will touch on some of these here and go into more

depth in an upcoming paper, especially regarding those less talked about

aspects related to tort law and negligence.

In

the laundry example, ultimately if we issued the LTX for our laundry

project we may be raising risk capital. Why? Because the economic

reality of this is that people are giving us money now to execute a

project where they will gain some benefit in the future, and this

benefit goes beyond a simple one off product or service. Unlike

reward-based crowdfunding, such as a Kickstarter campaign, the upside

for an ICO participant is not limited to receiving a single product or

service. An ICO participant is essentially buying into the on-going

commercial viability and success of the issuing company, and

participants anticipate that the value of the token(s) they own will

increase, in which case they can either earn a greater financial return

by selling the tokens (capital gains) or gain access to more services at

some discount (commercial benefits). Either way an ICO participant’s

expected returns may be seen as linked directly to the pooled funds of

the ICO and efforts of the issuer to use funds in executing the project

and ensuring viability of the ongoing business. It is this expectation

that drives participants to not only pay for a one-off product or

service (as they may on Kickstarter) but to buy into an ongoing

commercial proposition that is yet to be developed and commercialized,

and all for the expectation of some form of “unlimited”

(explicit/implicit) financial gain.

Due

to such complex economic realities of ICOs and the resulting appcoins,

it seems like these are a new form of asset class. If they do turn out

to be a new type of primitive security, then a decentralized model for

administration may be viable to ensure compliance with key client money

and asset rules. However, this is a discussion for another time.

While

the above complexities are related to statutory/policy/legal

challenges, if an ICO is seen as a public offering and the resulting

appcoin is considered a security, other less obvious challenges could

result from common law issues related to contract or tort violations.

These may become increasingly relevant as issuing companies expand and

become profitable, at which point they would become bigger targets for

consumer class action lawsuits. There may be legal risks related to

issues seen as violations of the ICO terms of contract, or other forms

of negligence directly linked to the losses suffered by token holders

e.g. if a price plummets to zero based on an issuers perceived

negligence. Such legal recourse may also become increasingly attractive

as an issuing company changes its business model, becomes successful,

and the tokens then become less relevant. This means that in the future

VCs/investors/acquirers will likely need to perform appropriate due

diligence related to such risks, thus impacting possible valuations for

growth companies.

Final Thought

We

must highlight that while the overview provided in this work is

speculative and dares to touch on things through a “thought experiment”

approach (a physicists and economists best friend) it is based on sound

financial, commercial and economic reasoning. The fact is that ICOs and

appcoins are a new phenomenon and while we may not have the benefits of

the Pachinko Parlor industry to look outside of our little bubble and

see what could be possible, we have our imagination, logic and

intellectual honesty to determine what is happening in this industry and

where it can go.

Many

are trying hard to believe, as well as convince others, that ICO tokens

are just like reward based crowdfunding or (absurdly) “paid API’s” [17]

in order to distance them from financial securities and or other forms

of economically complex financial innovations, only for the purposes of

abstracting legal and regulatory burdens. This may result in some

short-term gains but the chances are they may be missing a much (much)

bigger opportunity or even delaying a ticking time bomb.

ECCO PERCHE' QUESTA CRIPTOECONOMIA E' SOLO ALL'INIZIO

Urca, la faccenda si ingrossa oltre ogni aspettativa:

Putin Meets With Ethereum Founder To Create National Virtual Currency Vladimir Putin recently met with the founder of Ethereum, Vitalik Buterin, to discuss the potential use of Ethereum as a national virtual currency, one which would help Russia diversify its economy beyond oil and gas.

video sempre attualissimo

un grazie particolare a THE TREND SOCIAL

MERCATOLIBERO E' SU FACEBOOK: DIVENTA AMICO

clicca sull'immagine e vedrai il profilo. http://www.facebook.com/group.php?gid=52907831746

MICHELE NISTA: SOGGETTO PERICOLOSO

AVVERTENZA

Vi invito a leggere con molta attenzione quanto riportato: l' Accesso al Blog conferma che l' Utente ha letto e approvato le seguenti Avvertenze, liberando da qualsiasi Responsabilità il Blog come sottospecificato:Vi preghiamo di prendere atto che tutte le informazioni da me pubblicate non devono essere considerate una sollecitazione al pubblico risparmio. Tutti i Servizi pubblicati sul Sito o qualsiasi comunicazione devono essere intesi a titolo di esempio generale e a titolo di Informazione: poiché non possiamo conoscere le esigenze e la situazione patrimoniale di ogni Utente, non posso proporre sul Blog alcun tipo di consulenza personalizzata e dovrà essere cura di ogni visitatore adattare le informazioni e le proiezioni su qualsiasi Valore Mobiliare, da me indicate alla specifica situazione personale. In ogni caso non mi riterrò responsabili nei confronti di alcun utente o terze parti di alcun danno diretto o indiretto causato dall' uso delle informazioni fornite, da Strategie applicate, da dati Forniti, da eventuali mancanze nella completezza ed esattezza delle informazioni, da qualsiasi ritardo, imprecisione, errore, interruzione o omissione nella fornitura del servizio sulla Rete o in altri modi.Inoltre, in nessuna maniera, posso garantire che quanto da me previsto abbia, puntualmente, a verificarsi;Chiunque decida di seguire le mie indicazioni, lo fa sotto la sua totale ed esclusiva responsabilità. Come detto, non esiste alcuna garanzia che le mie opinioni siano sempre corrette;Il lettore deve decidere, sulla base delle sue conoscenze ed esperienze se, quando e come seguire le nie indicazioni per il futuro. La decisione finale, sarà sempre di sua esclusiva pertinenza;E' buona norma ricordarsi che il trading è una professione in cui pochi riescono a conseguire risultati mediamente positivi. Per contro, le probabilità di perdita in conto capitale sono molto alte e quindi non è ragionevole sottovalutarne i rischi.In nessun caso bisognerebbe assumere alcuna posizione di alcun tipo senza avere preventivamente posizionato uno stop-loss. Laddove non si sappia come e/o si fosse nell' impossibilità di collocarlo, consigliamo di astenersi dall'operazione.Chi non ha nè conoscenza teorica né tantomeno esperienza pratica di operazioni di Borsa, è da me caldamente sconsigliato ad intraprendere qualsiasi attività speculativa.Il Blog garantisce, infatti, che farà del proprio meglio per assicurare l'accuratezza e l'affidabilità del servizio, ponendo la massima diligenza nell'acquisizione ed elaborazione dei dati, ma non garantisce l'assoluta completezza ed esattezza né, tanto meno, la rispondenza rispetto all'andamento futuro delle quotazioni, o la non variabilità negativa del proprio capitale.Il Blog si riserva il diritto insindacabile di modificare in qualsiasi momento i Servizi offerti.Il Blog non avrà alcuna responsabilità per le eventuali perdite subite dall'Utente per aver utilizzato i dati contenuti nelle informazioni ricevute, per non aver compreso il metodo e/o per aver fatto affidamento sulle previsioni fornite. Eventuali risultati realizzati nel passato non costituiscono alcuna garanzia per il futuro. Il Blog non ha alcun legame di dipendenza o di relazione societaria con alcun gruppo bancario, finanziario, società quotata o intermediari. Il Blog inoltre non risponde per gli eventuali disservizi e/o pregiudizi che derivassero all'Utente per problemi dovuti all' hardware e al software utilizzati dall'Utente e/o dal programma di navigazione (browser) utilizzato per la connessione.Informativa Privacy Dlgs 196/2003Si comunica che tutte le informazioni trasmesse verranno utilizzate soltanto all' interno del Blog, esclusivamente ai fini della prestazione del servizio gratuito offerto e saranno divulgate unicamente ai soggetti incaricati dell' espletamento dei relativi obblighi di legge in materia contabile e fiscale; in nessun altro caso saranno note a terzi. Titolare del trattamento dei dati sono io, gestore del blog.

Cookies Policy

Cookies Policy

QUESTO E' UN SITO BLOGSPOT (GOOGLE)

E QUINDI SEGUIAMO LE POLITICHE DELLA

CASA MADRE GOOGLE IN TERMINI DI COOKIES. I cookie sono file di testo che vengono

temporaneamente memorizzati sul disco rigido

del computer ogni volta che si visita un sito web.

Quando si esplora il nostro sito alcune informazioni

vengono acquisite automaticamente a fini

statistici o informativi e consentono un miglior

servizio. Le informazioni potrebbero permettere

l’identificazione del visitatore.

Tra queste informazioni ci sono: l’indirizzo IP l’URL (Uniform Resource Identifier) delle

risorse richieste l’orario e la data della richiesta La tipologia di sistema operativo, il browser

utilizzato, la risoluzione dello schermo ed altre

informazioni tecniche Questi dati sono anonimi e vengono elaborati

e archiviati solo per fini statistici. Ci sono diversi tipi di Cookie, ognuno di essi

segue il comportamento degli utenti per

rendere l’esperienza complessiva più veloce,

più facile e più efficiente. I cookie non possono danneggiare il tuo

computer e non contengono informazioni

personali o riservate. Qui di seguito puoi trovare i tipi di cookie

utilizzati sul nostro sito e perché li usiamo: First-party Cookie: sono i cookie gestiti

direttamente dal sito internet in oggetto.

In genere sono i cookie necessari a raccogliere

informazioni statistiche sull’esperienza

dell’utente (durata della visita, numero

di click, etc.) e quelli relativi alla

personalizzazione della navigazione (form di login, personalizzazione della grafica, etc) Third-party Cookie: sono salvati sul

computer dell’utente da soggetti terzi, come

i social network e le agenzia di pubblicità.

La remarketing di Google Adwords, ad esempio,

salva dei cookies che scadono dopo un

numero definito di giorni e servono a

costruire segmenti di interessi basati sulle

pagine visitate dall’utente. Analytics Cookies: questi cookie vengono

utilizzati per misurare e analizzare come i

clienti utilizzano il nostro sito web.

Utilizziamo queste informazioni per migliorare

la vostra esperienza sul nostro sito. Altri cookie vengono utilizzati in forma

automatica per fornire servizi quali, a titolo

esemplificativo e non esaustivo, i banner

pubblicitari, la risposta agli articoli scritti,

l’invio di richieste di assistenza o informative.

La maggioranza dei browser web accetta

i cookie. Tuttavia si ha la possibilità di rifiutare i

cookies modificando le impostazioni del

tuo browser.

DISCLAIMER: Questo servizio e questo blog non costituiscono consulenza finanziaria né costituiscono sollecitazione al pubblico risparmio. Chi scrive declina ogni responsabilità su eventuali inesattezze dei dati riportati e chiunque investa i propri risparmi prendendo spunto dalle indicazioni riportate lo fa a proprio rischio e pericolo.E' possibile che chi scrive sia direttamente interessato in qualità di risparmiatore privato all'andamento dei valori mobiliari di cui si discute. (leggete la nota a fondo pagina)

1 commento:

Urca, la faccenda si ingrossa oltre ogni aspettativa:

Putin Meets With Ethereum Founder To Create National Virtual Currency

Vladimir Putin recently met with the founder of Ethereum, Vitalik Buterin, to discuss the potential use of Ethereum as a national virtual currency, one which would help Russia diversify its economy beyond oil and gas.

Posta un commento