LE RISERVE CINESI ANCORA IN CALO PESANTE A GENNAIO

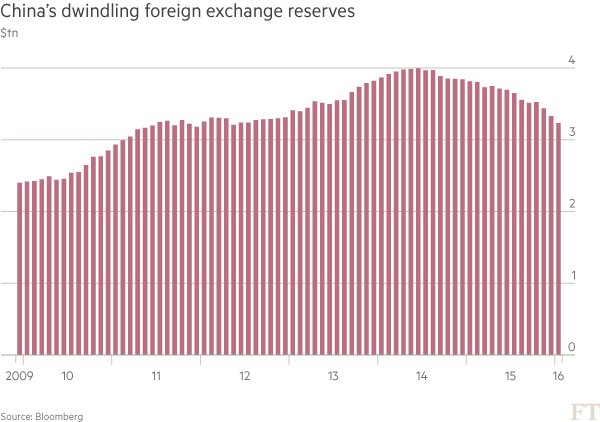

La cina ha appena annunciato la riduzione dele riserve di genaio: siamo a 3,23 trilion dollar (le attese erano per una discesa a 3,21) il mese scorso erano a 3,33.

Il calo continua a rimanere significativo e rappresenta la fatica della banca centrale cinese a difendere il valore dello YUAN.

La discesa del dollaro di questa settimana potrebbe attenuare il flusso ulteriormente in febbraio

SE COSI' NON FOSSE ..LA RIDUZIONE DELLE RISERVE ACCUMULATE POTREBBE OBBLIGARE LA CINA A SVALUTARE LO YUAN CON CONSEGUENZE CATASTROFICHE...100 MILIARDI AL MESE ..CON RISERVE PARI A 3,23 MILIARDI ...DAREBBERO SOLO 32 MESI DI SOPRAVVIVENZA PRIMA DI AZZERARE LE RISERVE VALUTARIE.

UN DOLLARO DEBOLE (ESSENDO IL DOLLARO PEGATO CON LO YUAN ....PER ORA....) AIUTA LA RIDUZIONE DEL PROCESSO DI EROSIONE DELLE RISERVE.

The PBOC is caught between the devil and the deep blue sea, facing a choice of either continued slow erosion of FX reserves, or a rapid currency adjustment that could be destabilizing for China and plunge global currency markets into turmoil. Further sharp yuan devaluation remains one of the key downside risks to the global economic outlook in 2016, due to the shock waves it will cause in global currency markets.

In such a downside risk scenario where the PBOC capitulates due to further rapid erosion of FX reserves and there is significant further yuan devaluation, this could also cause shocks in China’s corporate debt markets, as Chinese non-bank borrowers hold a large amount of USD debt, estimated at USD 1.2 trillion in mid-2015. The combination of moderating Chinese growth, excess capacity in key industries, rising USD yields and a potential further yuan slide against the USD all create risks of further stress for some Chinese corporate borrowers, which could trigger an increasing number of corporate debt defaults in 2016.

Iscriviti a:

Commenti sul post (Atom)

1 commento:

"La discesa del dollaro di questa settimana potrebbe attenuare il flusso ulteriormente in febbraio"

QUINDI.....?????????

Posta un commento